IT Asset Management IT Asset Management

How to Avoid a Pricey SAP Digital Access Surprise

14.05.2020 |

If you’re an SAP customer, you’re probably all too familiar with SAP’s encouragement to move...

SAP’s licensing revenue has changed. It is increasingly difficult for them to track and to charge for Indirect Access, in which you pay a Named User license for accessing SAP data via third-party.

This led to SAP® introducing a new licensing model in 2018. Digital Access has been promoted as a customer-friendly alternative to Indirect Access, and a straightforward way to calculate fees based on counting the documents you create in SAP systems.

But SAP is in the business of collecting revenue and Digital Access is a way to monetize your digital transformation. Let’s look at SAP’s recent changes to Estimation Reports and how they handle “subsequent documents” to determine whether Digital Access is cost effective for you.

At USU, we know from working with customers on successful audit defenses that SAP now has problems with justifying their Indirect Access license fees.

According to SAP agreements, all use of SAP software needs to be licensed, whether it is accessed directly via dialog or accessed indirectly via third-party upstream of a proprietary intermediary system.

That indirect access doesn’t necessarily result in licensable Indirect Access. In some cases, the functions being performed don’t constitute “Use” as described in the contracts. However, if it does qualify as Use, then you would need either a package license, a user license or in some cases both, in order to be compliant.

Indirect Access continues to be a major problem for companies who did not fully understand its implications or were not aware of licensing requirements when implementing new technologies. SAP is known for being aggressive with their audit tactics, often targeting Indirect Access in order to generate high licensing revenue (remember the infamous Diageo indirect access lawsuit).

This lack of understanding and the advent of automation and digitalization in recent times has made many customers easy prey.

Want to know more about SAP Digital Access?

Read our blog article "How to Avoid an Expensive Surprise with Digital Access."

The Digital Access licensing model is easier to define and easier to measure. It involves licensing your indirect access according to the number of Digital Documents entered into SAP via external third-party systems. There are nine SAP Digital Documents types including Sales & Purchase Orders, Financial Postings and Material Movements.

This licensing model can seem straightforward. You don’t have to count all the ways a person might access their SAP systems (like Named Users) or measure if those access points are directly through an SAP portal or third-party vendor (like Indirect Access).

And this model can work for you. Our USU team has seen many cases where Digital Access was the cheaper alternative for the customer.

But this model can also work against you. From our practical experience with customers, we can confirm that through Digital Access, existing scenarios that were compliant have suddenly become chargeable, which leads to those new SAP license revenue streams.

In our analyses for USU customers, the results varied significantly from case to case, regardless of the size of the company. So, it's critical to correctly identify if Digital Access will be a cost-effective model for your business.

One way to estimate your potential Digital Access costs is working with SAP´s Estimation Note. Their Global License Audit and Compliance (GLAC) team looks at your current document consumption and estimates what a year of document creation might cost under Digital Access.

Secretly and quietly, however, SAP has changed their Estimation Notes and Reports. For S/4HANA and ECC, there are new versions of the notes, and new reports under new names. The old notes are now classified as obsolete.

For details, see SAP Notes:

2992090 - Completely revised Digital Access estimation report 2 for ECC - Version 5 (3rd Dec. 2021)

2999672 - Completely revised Digital Access estimation report 2 for S/4H - Version 3 (19th Jan. 2021)

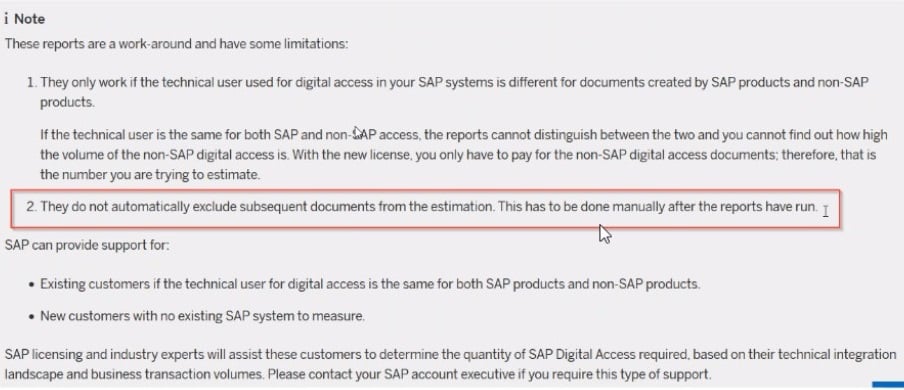

SAP’s counting and estimation included subsequent documents, which are non-chargeable repeats of new documents. But on help.sap.com, you can see this limitation: “They do not automatically exclude subsequent documents from the estimation. This has to be done manually after the reports have run.”

Uh oh. This means SAP’s Estimation Note will count all of your documents, including the “subsequent” repeating ones that do not require a fee. Then you must go through that estimation, identify those subsequent documents, remove them from the list, and recalculate the estimation. That’s a lot of manual work for an “automated” report.

We have talked about a complex and costly decision: How can SAP customers know if they should switch to Digital Access or keep their current contract for Indirect Access?

That’s why USU has built the industry’s first solution to simulate the logic of SAP's own Estimation Note. USU Software Asset Management provides a simplified method for calculating costs under Digital Access and accurately predicting the number of document licenses required. Our solution adds value by being more accurate and truly automated since we include important factors such as Financial subsequent documents.

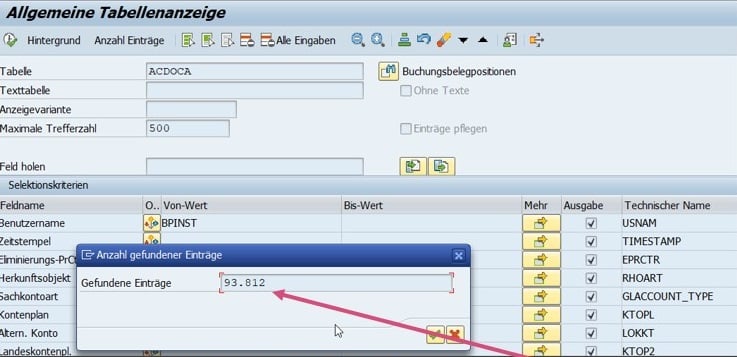

Here is an example of our Digital Access Estimator features as compared to SAP’s Estimation Note. The blue screenshot shows how SAP counts Financial documents in their Estimation Note. In this example, their total is 93, 812 documents.

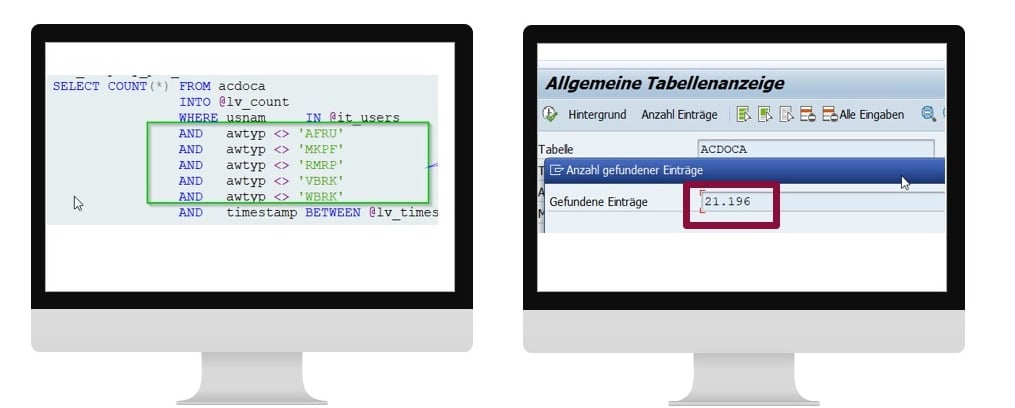

The white screenshot is how our USU solution counts the Financial documents initially, also at 93,812.

However, our solution then does something unique. It considers that Financial subsequent documents should be excluded, which, according to SAP, may not be counted.

This means our final calculation for Digital Access is only 21,196 documents, almost 80% fewer documents than originally counted in the old Estimation Note from SAP.

In fact, we have determined that Finance document types -- which can reach a considerable size and are therefore "only" charged at 20% (that is, multiplied by a factor of 0.2) – are overcounted by 62% on average.

Counts 80% fewer documents than SAP:

USU Software Asset Management is the first solution in the market to provide SAP customers with the complete overview and insight they need to make informed decisions about Digital Access.

If you are considering a move from Indirect Access, our Digital Access Estimator features calculate the true potential costs – including disregarding fees for non-chargeable subsequent Financial documents -- so you can evaluate properly.

If you have already purchased Digital Access licenses based on SAP’s Estimator Reports, then our analysis helps you to enter contract negotiations with SAP from a position of strength and achieve the best results.

Getting expert help can help you buy the right licenses at the right time at the right price and on the best conditions. If you are looking for experts to support your evaluation of Digital Access licensing, then don’t hesitate to get in touch with us.

Download our free white paper "SAP® Indirect vs. Digital Access" today and learn how to control risks and avoid unnecessary costs in SAP license management.

© 2021 SAP SE or an SAP group company. All rights reserved. SAP and other SAP products and services mentioned herein as well as their respective logos are trademarks or registered trademarks of SAP SE in Germany and other countries. All other names of products and services are trademarks of their respective companies. For additional trademark information and endorsements, please visit http://www.sap.com/trademark.

IT Asset Management IT Asset Management

If you’re an SAP customer, you’re probably all too familiar with SAP’s encouragement to move...

IT Asset Management IT Asset Management

You worry about SAP indirect access. Other SAP customers grumble about it. SAP promises to address...

Since it unveiled its document-basedDigital Accessmodel last year, SAP has been encouraging its...